Millennials: 1 in 6 now have $100,000 socked away

Adam Shell, USA TODAY

(Photo: LM Otero, AP)

Millennials are pushing back against the stereotype that their money management skills are lacking, as 16% now have savings of $100,000 or more, double the amount of young people who had socked away that much in 2015, according to a new Bank of America survey.

The perception that Millennials — Americans between the ages of 23 and 37 — lack savvy when it comes to saving for retirement, budgeting and setting up and sticking to a financial plan is showing signs of being outdated, noted the survey, made available exclusively to USA TODAY.

Despite many of these young Americans coming of age a decade ago during the worst financial crisis since the Great Depression and despite being saddled with high student loan debt, Millennials appear to be getting their financial lives in order and taking money matters more seriously.

Sixteen percent say they have $100,000 or more in savings, up from 8% in 2015. And nearly half (47%) have $15,000 socked away, up from 33% in 2015.

"Despite stereotypes of Millennials as being foolish with money and not long-term planners," they are actually behaving "quite responsibly" when it comes to money, says Andrew Plepler, global head of environmental, social and governance at Bank of America, summarizing the findings of the bank's 2018 Better Money Habits Millennial Report released Tuesday. "They deserve more credit. Millennials are actually doing better than you — and they — might think."

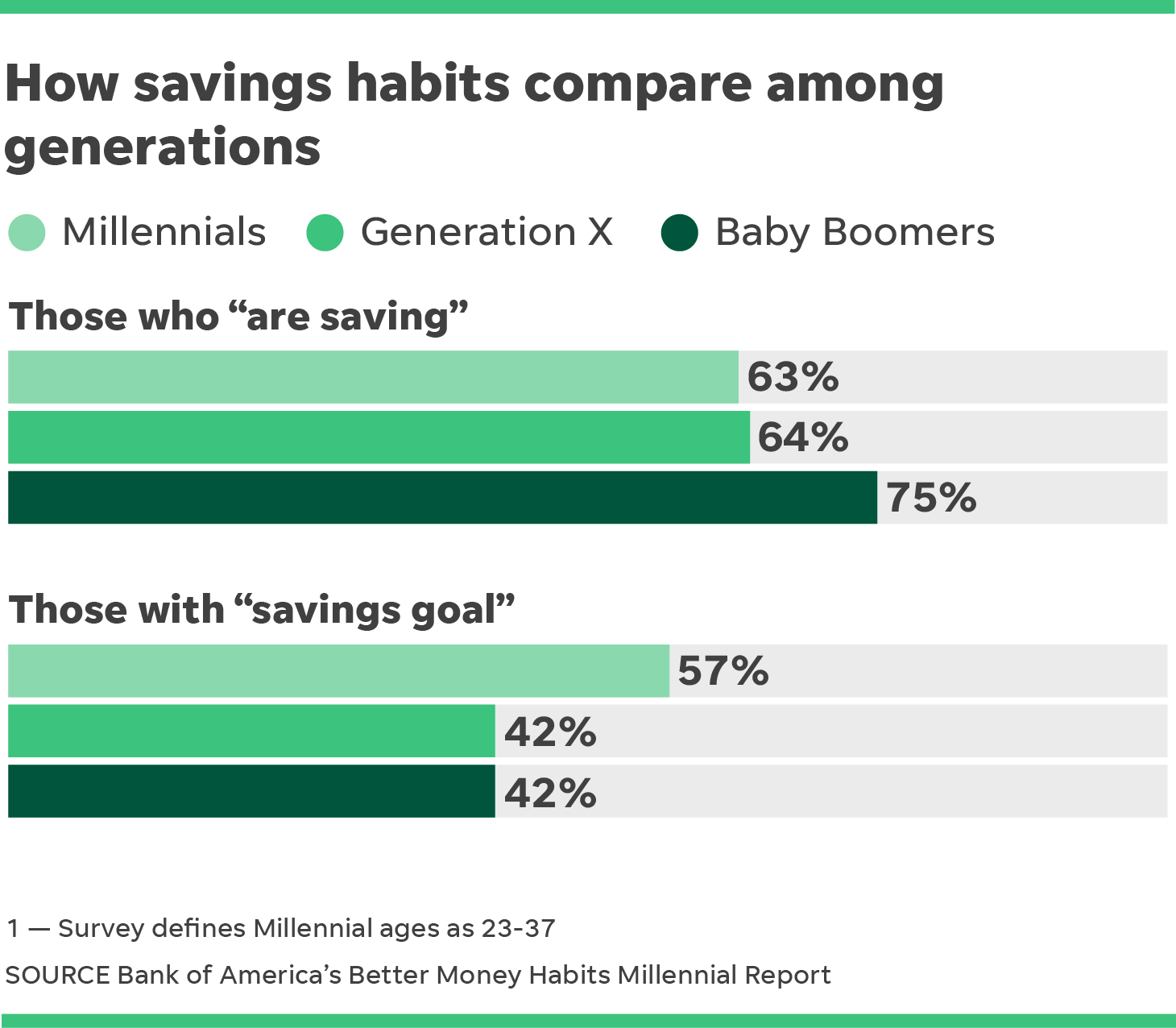

About two of three (63%) of Millennials surveyed say they "are saving," which is in line with 64% of Generation X but shy of 75% of Baby Boomers who set money aside.

More importantly, 54% of Millennials say they have a budget, with nearly three of four (73%) saying they stick to the budget each month. And another 57% say they have a "savings goal," which is higher than the 42% of Gen Xers and Boomers who say they are saving with a goal in mind.

Those better habits are translating into more sizable account balances — and more financial security.

About 60% say they "feel financially secure."

"Their financial habits have become more disciplined," Plepler says. "They've built it into their lifestyles."

Aside from saving for an emergency, which 64% said was a "top priority," half (49%) said saving for retirement and a third (33%) said saving to buy a house were their top savings goals.

Other key findings of BofA's Millennial survey, however, suggest this young generation still suffers from money-related angst and that there's still room for improvement in their cash-management skills.

The top financial "stressors" of Millennials, according to the survey, include:

* Not saving enough (35%).

* My career path (24%).

* Not planning and saving for retirement (21%).

* Not being able to afford a home (20%).

* Health costs (19%).

* Student loans; spending more than I should; credit-card debt; not having enough to invest; losing my job (17% for all).

One potential challenge for Millennials saving for retirement is the fact that one in four (26%) say they work in the "gig economy," or take on short-term contract work or freelance work. That means they likely don't have access to an employer-sponsored retirement account, such as a 401(k), and, as a result, they have to save on their own.

"These gig workers have to be more intentional about their saving," Plepler says. "The findings of our survey are encouraging, however. Millennials are taking much more proactive steps around saving. But this is an issue we have to monitor."

No comments:

Post a Comment